Thank you to arXiv for use of its open access interoperability.

Note: the date of arXiv entries announced right after publication holidays might incorrectly show up as the date of the publication holiday itself. This is due to our ad hoc method of inferring announcement dates, which are not returned by the arXiv API.

In this work, we study the worst-case to average-case hardness of the Learning with Errors problem (LWE) under an alternative measure of hardness - the maximum success probability achievable by a probabilistic polynomial-time (PPT) algorithm. Previous works by Regev (STOC 2005), Peikert (STOC 2009), and Brakerski, Peikert, Langlois, Regev, Stehle (STOC 2013) give worst-case to average-case reductions from lattice problems to LWE, specifically from the approximate decision variant of the Shortest Vector Problem (GapSVP) and the Bounded Distance Decoding (BDD) problem. These reductions, however, are lossy in the sense that even the strongest assumption on the worst-case hardness of GapSVP or BDD implies only mild hardness of LWE. Our alternative perspective gives a much tighter reduction and strongly relates the hardness of LWE to that of BDD. In particular, we show that under a reasonable assumption about the success probability of solving BDD via a PPT algorithm, we obtain a nearly tight lower bound on the highest possible success probability for solving LWE via a PPT algorithm. Furthermore, we show a tight relationship between the best achievable success probability by any PPT algorithm for decision-LWE to that of search-LWE. Our results not only refine our understanding of the computational complexity of LWE, but also provide a useful framework for analyzing the practical security implications.

In this work, we study the worst-case to average-case hardness of the Learning with Errors problem (LWE) under an alternative measure of hardness - the maximum success probability achievable by a probabilistic polynomial-time (PPT) algorithm. Previous works by Regev (STOC 2005), Peikert (STOC 2009), and Brakerski, Peikert, Langlois, Regev, Stehle (STOC 2013) give worst-case to average-case reductions from lattice problems to LWE, specifically from the approximate decision variant of the Shortest Vector Problem (GapSVP) and the Bounded Distance Decoding (BDD) problem. These reductions, however, are lossy in the sense that even the strongest assumption on the worst-case hardness of GapSVP or BDD implies only mild hardness of LWE. Our alternative perspective gives a much tighter reduction and strongly relates the hardness of LWE to that of BDD. In particular, we show that under a reasonable assumption about the success probability of solving BDD via a PPT algorithm, we obtain a nearly tight lower bound on the highest possible success probability for solving LWE via a PPT algorithm. Furthermore, we show a tight relationship between the best achievable success probability by any PPT algorithm for decision-LWE to that of search-LWE. Our results not only refine our understanding of the computational complexity of LWE, but also provide a useful framework for analyzing the practical security implications.

We show that there is a constant $k$ such that Buss's intuitionistic theory

$\mathsf{IS}^1_2$ does not prove that SAT requires co-nondeterministic circuits

of size at least $n^k$. To our knowledge, this is the first unconditional

unprovability result in bounded arithmetic in the context of worst-case

fixed-polynomial size circuit lower bounds. We complement this result by

showing that the upper bound $\mathsf{NP} \subseteq \mathsf{coNSIZE}[n^k]$ is

unprovable in $\mathsf{IS}^1_2$.

We show that there is a constant $k$ such that Buss's intuitionistic theory

$\mathsf{IS}^1_2$ does not prove that SAT requires co-nondeterministic circuits

of size at least $n^k$. To our knowledge, this is the first unconditional

unprovability result in bounded arithmetic in the context of worst-case

fixed-polynomial size circuit lower bounds. We complement this result by

showing that the upper bound $\mathsf{NP} \subseteq \mathsf{coNSIZE}[n^k]$ is

unprovable in $\mathsf{IS}^1_2$.

The Mermin-Peres magic square is a celebrated example of a system of Boolean

linear equations that is not (classically) satisfiable but is satisfiable via

linear operators on a Hilbert space of dimension four. A natural question is

then, for what kind of problems such a phenomenon occurs? Atserias, Kolaitis,

and Severini answered this question for all Boolean Constraint Satisfaction

Problems (CSPs): For 2-SAT, Horn-SAT, and Dual Horn-SAT, classical

satisfiability and operator satisfiability is the same and thus there is no

gap; for all other Boolean CSPs, the two notions differ as there is a gap,

i.e., there are unsatisfiable instances that are satisfied via operators on a

finite-dimensional Hilbert space. We generalize their result to CSPs on

arbitrary finite domains: CSPs of so-called bounded-width have no

satisfiability gap, whereas all other CSPs have a satisfiability gap.

The Mermin-Peres magic square is a celebrated example of a system of Boolean

linear equations that is not (classically) satisfiable but is satisfiable via

linear operators on a Hilbert space of dimension four. A natural question is

then, for what kind of problems such a phenomenon occurs? Atserias, Kolaitis,

and Severini answered this question for all Boolean Constraint Satisfaction

Problems (CSPs): For 2-SAT, Horn-SAT, and Dual Horn-SAT, classical

satisfiability and operator satisfiability is the same and thus there is no

gap; for all other Boolean CSPs, the two notions differ as there is a gap,

i.e., there are unsatisfiable instances that are satisfied via operators on a

finite-dimensional Hilbert space. We generalize their result to CSPs on

arbitrary finite domains: CSPs of so-called bounded-width have no

satisfiability gap, whereas all other CSPs have a satisfiability gap.

In this paper, we study conditions for the existence of an embedding

$\widetilde{f} \colon P \to Q \times \mathbb{R}$ such that $f = \mathrm{pr}_Q

\circ \widetilde{f}$, where $f \colon P \to Q$ is a piecewise linear map

between polyhedra. Our focus is on non-degenerate maps between graphs, where

non-degeneracy means that the preimages of points are finite sets.

We introduce combinatorial techniques and establish necessary and sufficient

conditions for the general case. Using these results, we demonstrate that the

problem of the existence of a lifting reduces to testing the satisfiability of

a 3-CNF formula. Additionally, we construct a counterexample to a result by V.

Po\'{e}naru on lifting of smooth immersions to embeddings.

Furthermore, by establishing connections between the stated problem and the

approximability by embeddings, we deduce that, in the case of generic maps from

a tree to a segment, a weaker condition becomes sufficient for the existence of

a lifting.

In this paper, we study conditions for the existence of an embedding

$\widetilde{f} \colon P \to Q \times \mathbb{R}$ such that $f = \mathrm{pr}_Q

\circ \widetilde{f}$, where $f \colon P \to Q$ is a piecewise linear map

between polyhedra. Our focus is on non-degenerate maps between graphs, where

non-degeneracy means that the preimages of points are finite sets.

We introduce combinatorial techniques and establish necessary and sufficient

conditions for the general case. Using these results, we demonstrate that the

problem of the existence of a lifting reduces to testing the satisfiability of

a 3-CNF formula. Additionally, we construct a counterexample to a result by V.

Po\'{e}naru on lifting of smooth immersions to embeddings.

Furthermore, by establishing connections between the stated problem and the

approximability by embeddings, we deduce that, in the case of generic maps from

a tree to a segment, a weaker condition becomes sufficient for the existence of

a lifting.

Authors: Taige Zhao, Jianxin Li, Ningning Cui, Wei Luo

Community search over heterogeneous information networks has been applied to

wide domains, such as activity organization and team formation. From these

scenarios, the members of a group with the same treatment often have different

levels of activity and workloads, which causes unfairness in the treatment

between active members and inactive members (called individual unfairness).

However, existing works do not pay attention to individual fairness and do not

sufficiently consider the rich semantics of HINs (e.g., high-order structure),

which disables complex queries. To fill the gap, we formally define the issue

of individual fairest community search over HINs (denoted as IFCS), which aims

to find a set of vertices from the HIN that own the same type, close

relationships, and small difference of activity level and has been demonstrated

to be NP-hard. To do this, we first develop an exploration-based filter that

reduces the search space of the community effectively. Further, to avoid

repeating computation and prune unfair communities in advance, we propose a

message-based scheme and a lower bound-based scheme. At last, we conduct

extensive experiments on four real-world datasets to demonstrate the

effectiveness and efficiency of our proposed algorithms, which achieve at least

X3 times faster than the baseline solution.

Community search over heterogeneous information networks has been applied to

wide domains, such as activity organization and team formation. From these

scenarios, the members of a group with the same treatment often have different

levels of activity and workloads, which causes unfairness in the treatment

between active members and inactive members (called individual unfairness).

However, existing works do not pay attention to individual fairness and do not

sufficiently consider the rich semantics of HINs (e.g., high-order structure),

which disables complex queries. To fill the gap, we formally define the issue

of individual fairest community search over HINs (denoted as IFCS), which aims

to find a set of vertices from the HIN that own the same type, close

relationships, and small difference of activity level and has been demonstrated

to be NP-hard. To do this, we first develop an exploration-based filter that

reduces the search space of the community effectively. Further, to avoid

repeating computation and prune unfair communities in advance, we propose a

message-based scheme and a lower bound-based scheme. At last, we conduct

extensive experiments on four real-world datasets to demonstrate the

effectiveness and efficiency of our proposed algorithms, which achieve at least

X3 times faster than the baseline solution.

Networks play an ubiquitous role in computer science and real-world

applications, offering multiple kind of information that can be retrieved with

adequate methods. With the continuous growing in the amount of data available,

networks are becoming larger day by day. Consequently, the tasks that were

easily achievable on smaller networks, often becomes impractical on huge amount

of data, either due to the high computational cost or due to the impracticality

to visualise corresponding data. Using distinctive node features to group large

amount of connected data into a limited number of clusters, hence represented

by a representative per cluster, proves to be a valuable approach. The

resulting contracted graphs are more manageable in size and can reveal

previously hidden characteristics of the original networks. Furthermore, in

many real-world use cases, a definition of cluster is intrinsic with the data,

eventually obtained with the injection of some expert knowledge represent by a

categorical function. Clusters then results in set of connected vertices taking

the same values in a finite set C. In the recent literature, Lombardi and

Onofri proposed a novel, fast, and easily parallelisable approach under the

name of $\gamma$-contraction to contract a graph given a categorical function.

In this work, we formally define such approach by providing a rigorous

mathematical definition of the problem, which, to the best of our knowledge,

was missing in the existing literature. Specifically, we explore the variadic

nature of the contraction operation and use it to introduce the weaker version

of the colour contraction, under the name of $\beta$-contraction, that the

algorithmic solution exploits. We finally dive into the details of the

algorithm and we provide a full assesment on its convergence complexity relying

on two constructive proofs that deeply unveil its mode of operation.

Networks play an ubiquitous role in computer science and real-world

applications, offering multiple kind of information that can be retrieved with

adequate methods. With the continuous growing in the amount of data available,

networks are becoming larger day by day. Consequently, the tasks that were

easily achievable on smaller networks, often becomes impractical on huge amount

of data, either due to the high computational cost or due to the impracticality

to visualise corresponding data. Using distinctive node features to group large

amount of connected data into a limited number of clusters, hence represented

by a representative per cluster, proves to be a valuable approach. The

resulting contracted graphs are more manageable in size and can reveal

previously hidden characteristics of the original networks. Furthermore, in

many real-world use cases, a definition of cluster is intrinsic with the data,

eventually obtained with the injection of some expert knowledge represent by a

categorical function. Clusters then results in set of connected vertices taking

the same values in a finite set C. In the recent literature, Lombardi and

Onofri proposed a novel, fast, and easily parallelisable approach under the

name of $\gamma$-contraction to contract a graph given a categorical function.

In this work, we formally define such approach by providing a rigorous

mathematical definition of the problem, which, to the best of our knowledge,

was missing in the existing literature. Specifically, we explore the variadic

nature of the contraction operation and use it to introduce the weaker version

of the colour contraction, under the name of $\beta$-contraction, that the

algorithmic solution exploits. We finally dive into the details of the

algorithm and we provide a full assesment on its convergence complexity relying

on two constructive proofs that deeply unveil its mode of operation.

Authors: Bo Li, Lijun Li, Minming Li, Ruilong Zhang

We study a public event scheduling problem, where multiple public events are

scheduled to coordinate the availability of multiple agents. The availability

of each agent is determined by solving a separate flexible interval job

scheduling problem, where the jobs are required to be preemptively processed.

The agents want to attend as many events as possible, and their agreements are

considered to be the total length of time during which they can attend these

events. The goal is to find a schedule for events as well as the job schedule

for each agent such that the total agreement is maximized.

We first show that the problem is NP-hard, and then prove that a simple

greedy algorithm achieves $\frac{1}{2}$-approximation when the whole timeline

is polynomially bounded. Our method also implies a

$(1-\frac{1}{e})$-approximate algorithm for this case. Subsequently, for the

general timeline case, we present an algorithmic framework that extends a

$\frac{1}{\alpha}$-approximate algorithm for the one-event instance to the

general case that achieves $\frac{1}{\alpha+1}$-approximation. Finally, we give

a polynomial time algorithm that solves the one-event instance, and this

implies a $\frac{1}{2}$-approximate algorithm for the general case.

We study a public event scheduling problem, where multiple public events are

scheduled to coordinate the availability of multiple agents. The availability

of each agent is determined by solving a separate flexible interval job

scheduling problem, where the jobs are required to be preemptively processed.

The agents want to attend as many events as possible, and their agreements are

considered to be the total length of time during which they can attend these

events. The goal is to find a schedule for events as well as the job schedule

for each agent such that the total agreement is maximized.

We first show that the problem is NP-hard, and then prove that a simple

greedy algorithm achieves $\frac{1}{2}$-approximation when the whole timeline

is polynomially bounded. Our method also implies a

$(1-\frac{1}{e})$-approximate algorithm for this case. Subsequently, for the

general timeline case, we present an algorithmic framework that extends a

$\frac{1}{\alpha}$-approximate algorithm for the one-event instance to the

general case that achieves $\frac{1}{\alpha+1}$-approximation. Finally, we give

a polynomial time algorithm that solves the one-event instance, and this

implies a $\frac{1}{2}$-approximate algorithm for the general case.

Finding maximum cliques in large networks is a challenging combinatorial

problem with many real-world applications. We present a fast algorithm to

achieve the exact solution for the maximum clique problem in large sparse

networks based on efficient graph decomposition. A bunch of effective

techniques is being used to greatly prune the graph and a novel concept called

Complete-Upper-Bound-Induced Subgraph (CUBIS) is proposed to ensure that the

structures with the potential to form the maximum clique are retained in the

process of graph decomposition. Our algorithm first pre-prunes peripheral

nodes, subsequently, one or two small-scale CUBISs are constructed guided by

the core number and current maximum clique size. Bron-Kerbosch search is

performed on each CUBIS to find the maximum clique. Experiments on 50 empirical

networks with a scale of up to 20 million show the CUBIS scales are largely

independent of the original network scale. This enables an approximately linear

runtime, making our algorithm amenable for large networks. Our work provides a

new framework for effectively solving maximum clique problems on massive sparse

graphs, which not only makes the graph scale no longer the bottleneck but also

shows some light on solving other clique-related problems.

Finding maximum cliques in large networks is a challenging combinatorial

problem with many real-world applications. We present a fast algorithm to

achieve the exact solution for the maximum clique problem in large sparse

networks based on efficient graph decomposition. A bunch of effective

techniques is being used to greatly prune the graph and a novel concept called

Complete-Upper-Bound-Induced Subgraph (CUBIS) is proposed to ensure that the

structures with the potential to form the maximum clique are retained in the

process of graph decomposition. Our algorithm first pre-prunes peripheral

nodes, subsequently, one or two small-scale CUBISs are constructed guided by

the core number and current maximum clique size. Bron-Kerbosch search is

performed on each CUBIS to find the maximum clique. Experiments on 50 empirical

networks with a scale of up to 20 million show the CUBIS scales are largely

independent of the original network scale. This enables an approximately linear

runtime, making our algorithm amenable for large networks. Our work provides a

new framework for effectively solving maximum clique problems on massive sparse

graphs, which not only makes the graph scale no longer the bottleneck but also

shows some light on solving other clique-related problems.

Hairpin completion, derived from the hairpin formation observed in DNA

biochemistry, is an operation applied to strings, particularly useful in DNA

computing. Conceptually, a right hairpin completion operation transforms a

string $S$ into $S\cdot S'$ where $S'$ is the reverse complement of a prefix of

$S$. Similarly, a left hairpin completion operation transforms a string $S$

into $S'\cdot S$ where $S'$ is the reverse complement of a suffix of $S$. The

hairpin completion distance from $S$ to $T$ is the minimum number of hairpin

completion operations needed to transform $S$ into $T$. Recently Boneh et al.

showed an $O(n^2)$ time algorithm for finding the hairpin completion distance

between two strings of length at most $n$. In this paper we show that for any

$\varepsilon>0$ there is no $O(n^{2-\varepsilon})$-time algorithm for the

hairpin completion distance problem unless the Strong Exponential Time

Hypothesis (SETH) is false. Thus, under SETH, the time complexity of the

hairpin completion distance problem is quadratic, up to sub-polynomial factors.

Hairpin completion, derived from the hairpin formation observed in DNA

biochemistry, is an operation applied to strings, particularly useful in DNA

computing. Conceptually, a right hairpin completion operation transforms a

string $S$ into $S\cdot S'$ where $S'$ is the reverse complement of a prefix of

$S$. Similarly, a left hairpin completion operation transforms a string $S$

into $S'\cdot S$ where $S'$ is the reverse complement of a suffix of $S$. The

hairpin completion distance from $S$ to $T$ is the minimum number of hairpin

completion operations needed to transform $S$ into $T$. Recently Boneh et al.

showed an $O(n^2)$ time algorithm for finding the hairpin completion distance

between two strings of length at most $n$. In this paper we show that for any

$\varepsilon>0$ there is no $O(n^{2-\varepsilon})$-time algorithm for the

hairpin completion distance problem unless the Strong Exponential Time

Hypothesis (SETH) is false. Thus, under SETH, the time complexity of the

hairpin completion distance problem is quadratic, up to sub-polynomial factors.

In a pair of recent breakthroughs \cite{CHR,Li} it was shown that the classes $S_2^E, ZPE^{NP}$, and $\Sigma_2^E$ require exponential circuit complexity, giving the first unconditional improvements to a classical result of Kannan. These results were obtained by designing a surprising new algorithm for the total search problem Range Avoidance: given a circuit $C: \{0,1\}^n \to \{0,1\}^{n+1}$, find an $n+1$-bit string outside its range. Range Avoidance is a member of the class $TF\Sigma_2^P$ of total search problems in the second level of the polynomial hierarchy, analogous to its better-known counterpart $TFNP$ in the first level. $TF\Sigma_2^P$ was only recently introduced in \cite{KKMP} and its structure is not well understood. We investigate here the extent to which algorithms of the kind in \cite{CHR,Li} can be applied to other search problems in this class, and prove a variety of results both positive and negative.

On the positive side we show that Li's Range Avoidance algorithm \cite{Li} can be improved to give a reduction from Range Avoidance to a natural total search problem we call the Linear Ordering Principle or ``LOP'': given a circuit $\prec:\{0,1\}^n \times \{0,1\}^n \to \{0,1\}$ purportedly defining a total order on $\{0,1\}^n$, find either a witness that $\prec$ is not a total order or else a minimal element in the ordering. The problem LOP is quite interesting in its own right, as it defines a natural syntactic subclass ``$L_2^P$'' of $S_2^P$ which nonetheless maintains most of the interesting properties of $S_2^P$; in particular we show that $L_2^P$ contains $MA$ and that its exponential analogue ${L_2^E}$ requires $2^n/n$ size circuits. Both of these are consequences of our reduction from Range Avoidance to LOP.

On the negative side we prove that the algorithms developed in \cite{CHR,Li} cannot be extended to Strong Range Avoidance, a problem considered in the same paper which first introduced Range Avoidance \cite{KKMP}. In this problem we are given a circuit $C: \{0,1\}^n \setminus\{0^n\} \to \{0,1\}^n$, and once again seek a point outside its range. We give a separation in the decision tree (oracle) model showing that this problem cannot be solved in ${FP^{\Sigma_2^P}_{||}}$, which in particular rules out all of the new kinds of algorithms considered in \cite{CHR,Li}. This black box separation is derived from a novel depth 3 ${AC^0}$ circuit lower bound for a total search problem, which we believe is of independent interest from the perspective of circuit complexity: we show that unlike previous depth 3 lower bounds, ours cannot be proven by reduction from a decision problem, and thus requires new techniques specifically tailored to total search problems. Proving lower bounds of this kind was recently proposed by Vyas and Williams in the context of the original (Weak) Avoid problem.

In a pair of recent breakthroughs \cite{CHR,Li} it was shown that the classes $S_2^E, ZPE^{NP}$, and $\Sigma_2^E$ require exponential circuit complexity, giving the first unconditional improvements to a classical result of Kannan. These results were obtained by designing a surprising new algorithm for the total search problem Range Avoidance: given a circuit $C: \{0,1\}^n \to \{0,1\}^{n+1}$, find an $n+1$-bit string outside its range. Range Avoidance is a member of the class $TF\Sigma_2^P$ of total search problems in the second level of the polynomial hierarchy, analogous to its better-known counterpart $TFNP$ in the first level. $TF\Sigma_2^P$ was only recently introduced in \cite{KKMP} and its structure is not well understood. We investigate here the extent to which algorithms of the kind in \cite{CHR,Li} can be applied to other search problems in this class, and prove a variety of results both positive and negative.

On the positive side we show that Li's Range Avoidance algorithm \cite{Li} can be improved to give a reduction from Range Avoidance to a natural total search problem we call the Linear Ordering Principle or ``LOP'': given a circuit $\prec:\{0,1\}^n \times \{0,1\}^n \to \{0,1\}$ purportedly defining a total order on $\{0,1\}^n$, find either a witness that $\prec$ is not a total order or else a minimal element in the ordering. The problem LOP is quite interesting in its own right, as it defines a natural syntactic subclass ``$L_2^P$'' of $S_2^P$ which nonetheless maintains most of the interesting properties of $S_2^P$; in particular we show that $L_2^P$ contains $MA$ and that its exponential analogue ${L_2^E}$ requires $2^n/n$ size circuits. Both of these are consequences of our reduction from Range Avoidance to LOP.

On the negative side we prove that the algorithms developed in \cite{CHR,Li} cannot be extended to Strong Range Avoidance, a problem considered in the same paper which first introduced Range Avoidance \cite{KKMP}. In this problem we are given a circuit $C: \{0,1\}^n \setminus\{0^n\} \to \{0,1\}^n$, and once again seek a point outside its range. We give a separation in the decision tree (oracle) model showing that this problem cannot be solved in ${FP^{\Sigma_2^P}_{||}}$, which in particular rules out all of the new kinds of algorithms considered in \cite{CHR,Li}. This black box separation is derived from a novel depth 3 ${AC^0}$ circuit lower bound for a total search problem, which we believe is of independent interest from the perspective of circuit complexity: we show that unlike previous depth 3 lower bounds, ours cannot be proven by reduction from a decision problem, and thus requires new techniques specifically tailored to total search problems. Proving lower bounds of this kind was recently proposed by Vyas and Williams in the context of the original (Weak) Avoid problem.

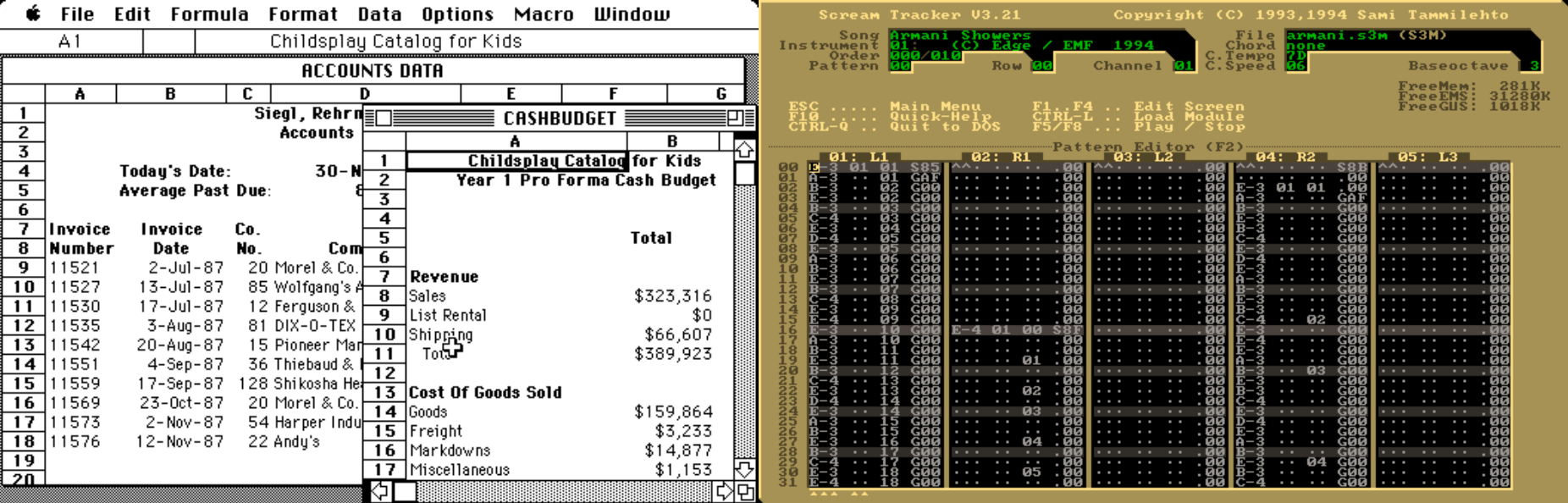

The long strange relationship between electronic music and business machines.

As a budding music nerd, I got pulled into the world of electronic music after discovering Scream Tracker in high school. I had been recording my various bands with a 4-track but wanted to try some more experimental directions. My summer job at the time was helping organize some logistical workbooks for the neurology department where my dad worked. It’s funny to look back at Scream Tracker and 90s-era Microsoft Excel next to each other. For me, computer music has always been doing clerical data entry into a spreadsheet.

Having grown up in the shadow of the business machine, electronic music has always had this bizarre bureaucratic dressing. Ironically, the dominant mode of transmitting creative ideas into computer music is the keyboard, and it’s not clear from context to which homonym I’m referring. Do I mean the one with letters or the one with white and black keys? Why not both?

Look at drum machines. We took our most visceral instruments—percussion you physically pummel to summon massive grooves—and put them in a box that looks like an answering machine.

And yet these boxes can move a club in ways a drummer never could.

Mechanical business machines could conjure the most intense human emotions. Our spreadsheet samplers and a single drum loop created an alien genre that still gets people moving today.

But it always seemed like these music tools were a technological crutch and that the real future of music would be bringing the sonic versatility of electronic music back to the old physical reality of banging on things to get people to dance. Wouldn’t people soon tire of going to shows to watch people turn knobs?

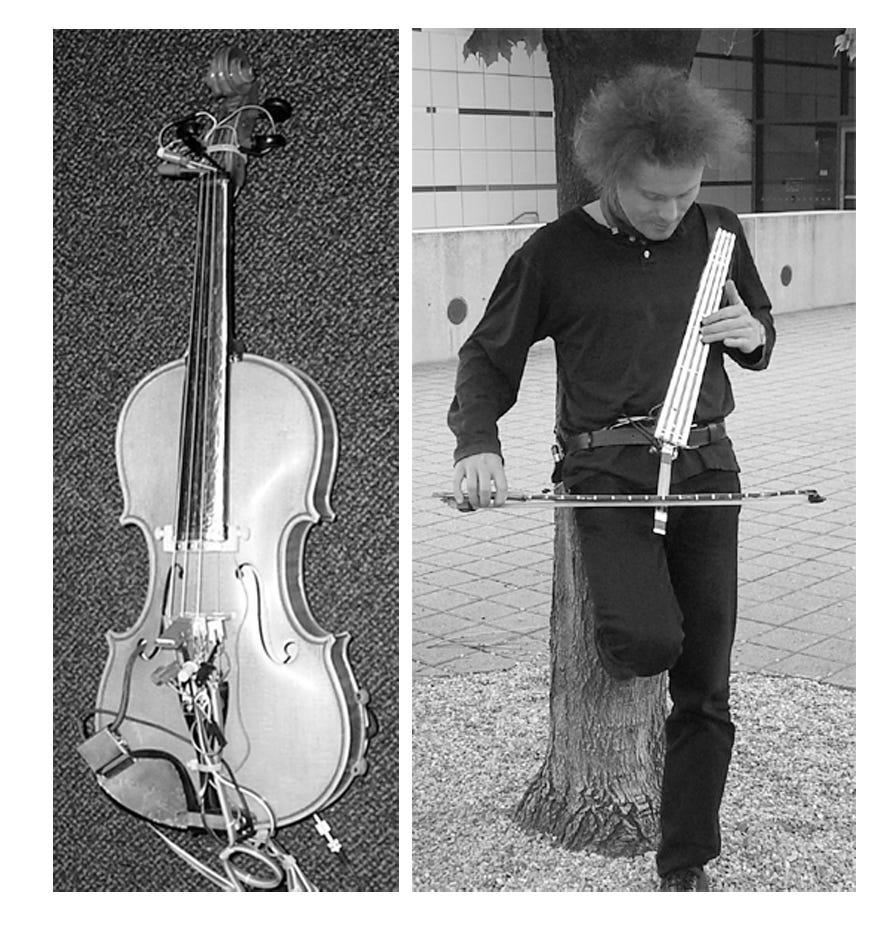

Ostensibly, I was admitted to graduate school to work on AI for music. I guess we didn’t call it AI at the time, because AI was a dirty word in the year 2000 (footnote It still should be a dirty word, damn it!). My lab had developed what my advisor, Neil Gershenfeld, called a “Digital Stradivarius.” Neil figured that as long as you could sample the sonic timbre of a genuine Stradivarius, you could use machine learning to synthesize the nuances of playing a real one. Bernd Schoner’s PhD used expectation maximization and some clever hardware to make a pretty nice-sounding digital cello. He called it a “marching cello” as it was far less bulky than its analog counterpart:

But as software improved, I quickly became disenchanted with musical hardware. More and more devices could be replaced by your laptop. By the early 2000s, I could, on the same computer, record and mix a rock band, make upbeat techno, and create live ambient music. Though die-hards hold onto their room-sized modular synthesizers, we crossed the laptop singularity decades ago.

Fast forward to 2024, the most dominant tool for electronic music production and beyond is the software Ableton Live. I have been a committed Live user since the beta tests in 2001. Though it initially just played looping samples, it now has impressive synthesis engines, support for programming your own plug-ins, and a built-in search engine for managing your library of sounds.

25 years later, we don’t have a better marching cello, but we have an amazing Stradivarius sample pack. It turned out that samples were all you need. You didn’t need machine learning. And instead of a novel device for bowing and nuanced articulation, you still input commands like you did in 1999. Enter the data with a keyboard and mouse into a spreadsheet:

But if the future of music is the same as the future of the spreadsheet, what does that say about the future of AI and music? Maybe that means we should look at which areas LLMs are supposedly going to revolutionize and think about how to directly map those applications onto computer music.

As you, my dear readers, know, I don’t think LLMs are going to walk, talk, see, write, reproduce themselves, or be conscious of their existence. But I also don’t think they are useless. In particular, the most compelling and impressive application of large language models thus far has been code generation. The sorts of projects graduate students can build with GPT4 are beyond impressive. What would the analog be in music? As I wrote on Monday and hint at today, the most challenging part of modern digital audio is making sense of the infinite collection of synthesizer presets and sample packs.

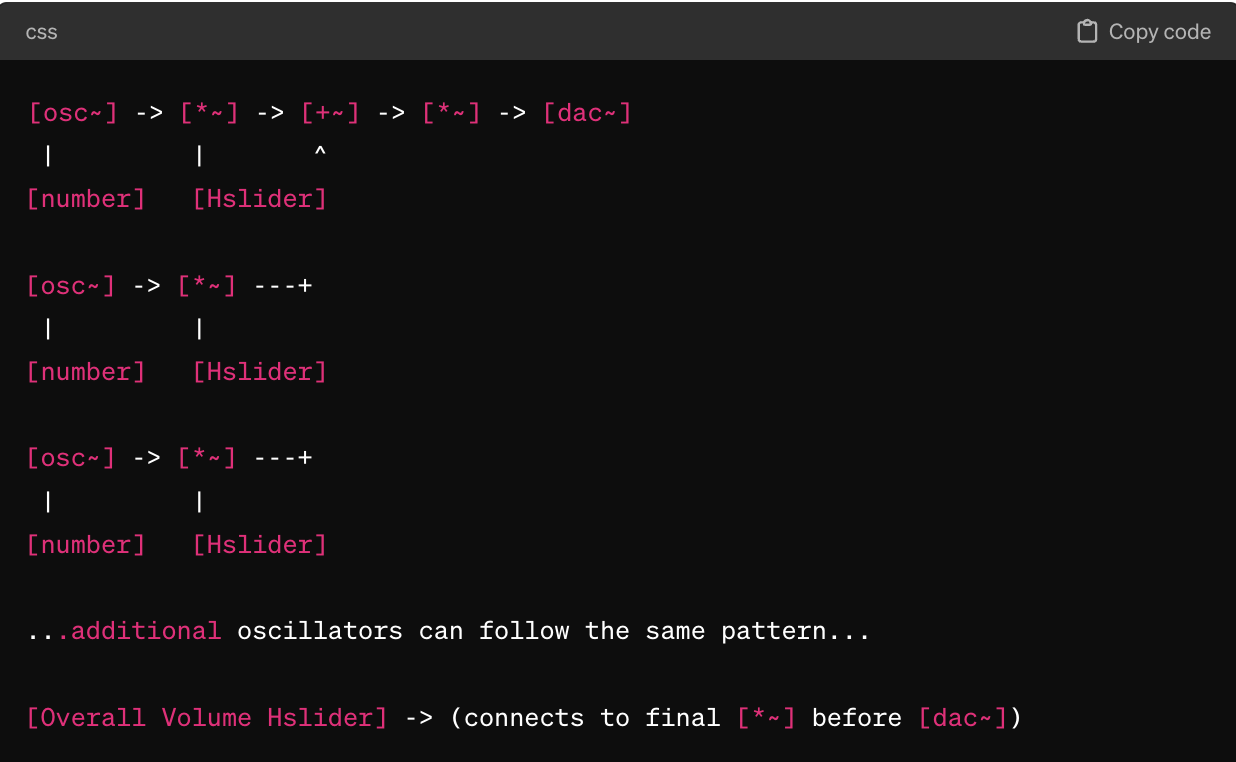

At its most abstract level, could we create a prompt system for synthesizers? People can make incredible music with the graphical programming language MaxMSP. Can we simplify creating MaxMSP patches with GPT4? MaxMSP is just code, after all! This isn’t that far away from what I can tell. GPT4 knows what pd is (it’s the open source version of MaxMSP), and it can sort of help you get started building patches. I asked it to create a pd patch of a simple additive synthesizer, and it gave me a long spiel and “a simplified textual diagram of what the patch might look like.”

Tightening this up seems pretty straightforward, doesn't it?

Moving from code to information retrieval, could we build better search tools for the vast collection of sounds we now have access to? Ableton Live ships with gigabytes of presets, and finding the one you have in mind can take hours. Can we build a chatbot that helps us navigate the infinite sea of sounds? As it exists now, the search capabilities in software like Ableton Live only index the keywords in the names of the presets. What if they could get access to more metadata? Perhaps search could then return a list of instruments and plugins associated with a natural language prompt. More ambitiously, what about sound search? Could we take a sample of music and suggest sample packs that might get you close to emulating the style? Bringing richer data to this search could open up endless creative possibilities.

Another idea that’s probably within our reach is converting existing songs into playable instruments. Ableton Live already has an “audio to midi” converter that takes sounds and converts the melody and rhythm into primitive computer music code. Could better AI tooling take a recording and produce a sampler instrument that recreates something that approximates the input’s nuance? Maybe we could upload a band’s recording, extract melodies and rhythms of the different players, and give continuous control parameters that the producer could manipulate. Where are we with source separation technology?

The issue with my wishlist is music remains a low-margin business. Listening, playing, and dancing to music are fundamental to our lives, but you’re not going to get a big VC check to innovate them. So a last question: Can you build the sorts of projects I’m asking about using cheap, open-source models? My guess is you can! And someone really should.

For our next favorite theorem, we look at the surprising power of provers who share entangled bits. If you can prove something to an arbitrarily computable verifier, then two entangled provers can convince a polynomial-time verifier.

MIP* = RE Zhengfeng Ji, Anand Natarajan, Thomas Vidick, John Wright and Henry Yuen

A quick tour:

A powerful prover convincing a skeptical computable deterministic verifier is another way of capturing computably enumerable (traditionally called recursively enumerable or RE). You can convince a verifier that a program halts by giving the halting time, and the verifier can simulate the machine for that many steps.

A powerful prover convincing a skeptical polytime deterministic verifier is another way of capturing the class NP, like giving a 3-coloring of a graph that can be easily checked.

If you allow the verifier to ask random questions, you can convince the verifier with high confidence that a graph is not colorable, or more generally any PSPACE problem.

If you add two separated provers that a skeptical probabilistic verifier can play off each other, the provers can convince the verifier that any problem in NEXP, non-deterministic exponential time.

One of many quantum variations of interactive proofs, MIP* has two provers that cannot communicate but have entangled quantum bits. This change could go either way:

The provers to coordinate their answers better and so they wouldn't convince the verifier for all the languages in NEXP

The verifier could ask more complex questions to the provers which they could answer using the entanglement, allowing the provers to convince the verifier for even more complex languages.

Turns out it's the later in a very strong way.

Ito and Vidick showed that you can create a protocol that prevents the provers coordinating better, recovering all problems in NEXP. Vidick and Wright showed you can ask more questions, showing that provers with entangled bits can convince a verifier of everything in NEEXP, non-deterministic double exponential time (\(2^{2^{n^c}}\)), already a proof too large for the verifier to even point into. The MIP* = RE paper takes that all the way to the computably enumerable sets, all the languages you would get with a classical prover convincing a deterministic verifier unrestricted by time.

By Lance Fortnow

For our next favorite theorem, we look at the surprising power of provers who share entangled bits. If you can prove something to an arbitrarily computable verifier, then two entangled provers can convince a polynomial-time verifier.

MIP* = RE Zhengfeng Ji, Anand Natarajan, Thomas Vidick, John Wright and Henry Yuen

A quick tour:

A powerful prover convincing a skeptical computable deterministic verifier is another way of capturing computably enumerable (traditionally called recursively enumerable or RE). You can convince a verifier that a program halts by giving the halting time, and the verifier can simulate the machine for that many steps.

A powerful prover convincing a skeptical polytime deterministic verifier is another way of capturing the class NP, like giving a 3-coloring of a graph that can be easily checked.

If you allow the verifier to ask random questions, you can convince the verifier with high confidence that a graph is not colorable, or more generally any PSPACE problem.

If you add two separated provers that a skeptical probabilistic verifier can play off each other, the provers can convince the verifier that any problem in NEXP, non-deterministic exponential time.

One of many quantum variations of interactive proofs, MIP* has two provers that cannot communicate but have entangled quantum bits. This change could go either way:

The provers to coordinate their answers better and so they wouldn't convince the verifier for all the languages in NEXP

The verifier could ask more complex questions to the provers which they could answer using the entanglement, allowing the provers to convince the verifier for even more complex languages.

Turns out it's the later in a very strong way.

Ito and Vidick showed that you can create a protocol that prevents the provers coordinating better, recovering all problems in NEXP. Vidick and Wright showed you can ask more questions, showing that provers with entangled bits can convince a verifier of everything in NEEXP, non-deterministic double exponential time (\(2^{2^{n^c}}\)), already a proof too large for the verifier to even point into. The MIP* = RE paper takes that all the way to the computably enumerable sets, all the languages you would get with a classical prover convincing a deterministic verifier unrestricted by time.

April 18-30, 2024 Vancouver, Canada sigact.org/tcsforall/ Submission deadline: April 28, 2024 Nomination deadline for TCS for All Spotlight Workshop and travel scholarships to attend STOC are on April 28th. Nominate your students and postdocs who will be in the job market in near future. Since 2018, TCS for All (previously TCS for Women) is supporting … Continue reading TCS for All Rising Star Workshop and Travel Scholarships

By shacharlovett

April 18-30, 2024 Vancouver, Canada https://sigact.org/tcsforall/ Submission deadline: April 28, 2024 Nomination deadline for TCS for All Spotlight Workshop and travel scholarships to attend STOC are on April 28th. Nominate your students and postdocs who will be in the job market in near future. Since 2018, TCS for All (previously TCS for Women) is supporting … Continue reading TCS for All Rising Star Workshop and Travel Scholarships

One of the elegant achievements in the history of proof theory is the

characterization of the provably total recursive functions of an arithmetical

theory by its proof-theoretic ordinal as a way to measure the time complexity

of the functions. Unfortunately, the machinery is not sufficiently fine-grained

to be applicable on the weak theories on the one hand and to capture the

bounded functions with bounded definitions of strong theories, on the other. In

this paper, we develop such a machinery to address the bounded theorems of both

strong and weak theories of arithmetic. In the first part, we provide a refined

version of ordinal analysis to capture the feasibly definable and bounded

functions that are provably total in $\mathrm{PA}+\bigcup_{\beta \prec \alpha}

\mathrm{TI}(\prec_{\beta})$, the extension of Peano arithmetic by transfinite

induction up to the ordinals below $\alpha$. Roughly speaking, we identify the

functions as the ones that are computable by a sequence of

$\mathrm{PV}$-provable polynomial time modifications on an initial polynomial

time value, where the computational steps are indexed by the ordinals below

$\alpha$, decreasing by the modifications. In the second part, and choosing $l

\leq k$, we use similar technique to capture the functions with bounded

definitions in the theory $T^k_2$ (resp. $S^k_2$) as the functions computable

by exponentially (resp. polynomially) long sequence of

$\mathrm{PV}_{k-l+1}$-provable reductions between $l$-turn games starting with

an explicit $\mathrm{PV}_{k-l+1}$-provable winning strategy for the first game.

One of the elegant achievements in the history of proof theory is the

characterization of the provably total recursive functions of an arithmetical

theory by its proof-theoretic ordinal as a way to measure the time complexity

of the functions. Unfortunately, the machinery is not sufficiently fine-grained

to be applicable on the weak theories on the one hand and to capture the

bounded functions with bounded definitions of strong theories, on the other. In

this paper, we develop such a machinery to address the bounded theorems of both

strong and weak theories of arithmetic. In the first part, we provide a refined

version of ordinal analysis to capture the feasibly definable and bounded

functions that are provably total in $\mathrm{PA}+\bigcup_{\beta \prec \alpha}

\mathrm{TI}(\prec_{\beta})$, the extension of Peano arithmetic by transfinite

induction up to the ordinals below $\alpha$. Roughly speaking, we identify the

functions as the ones that are computable by a sequence of

$\mathrm{PV}$-provable polynomial time modifications on an initial polynomial

time value, where the computational steps are indexed by the ordinals below

$\alpha$, decreasing by the modifications. In the second part, and choosing $l

\leq k$, we use similar technique to capture the functions with bounded

definitions in the theory $T^k_2$ (resp. $S^k_2$) as the functions computable

by exponentially (resp. polynomially) long sequence of

$\mathrm{PV}_{k-l+1}$-provable reductions between $l$-turn games starting with

an explicit $\mathrm{PV}_{k-l+1}$-provable winning strategy for the first game.

Automaton learning is a domain in which the target system is inferred by the

automaton learning algorithm in the form of an automaton, by synthesizing a

finite number of inputs and their corresponding outputs. Automaton learning

makes use of a Minimally Adequate Teacher (MAT). The learner learns the target

system by posing membership queries to the MAT. In this chapter, I have

provided completely solved examples of automaton learning algorithms. According

to the best of my knowledge these are not available in any other source.

Automaton learning is a domain in which the target system is inferred by the

automaton learning algorithm in the form of an automaton, by synthesizing a

finite number of inputs and their corresponding outputs. Automaton learning

makes use of a Minimally Adequate Teacher (MAT). The learner learns the target

system by posing membership queries to the MAT. In this chapter, I have

provided completely solved examples of automaton learning algorithms. According

to the best of my knowledge these are not available in any other source.

We prove optimal concentration of measure for lifted functions on high

dimensional expanders (HDX). Let $X$ be a $k$-dimensional HDX. We show for any

$i\leq k$ and $f:X(i)\to [0,1]$: \[\Pr_{s\in

X(k)}\left[\left|\underset{{t\subseteq

s}}{\mathbb{E}}[f(t)]-\mu\right|\geq\varepsilon\right]\leq

exp\left(-\varepsilon^2\frac{k}{i}\right).\] Using this fact, we prove that

high dimensional expanders are reverse hypercontractive, a powerful functional

inequality from discrete analysis implying that for any sets $A,B \subset

X(k)$, the probability a $\rho$-correlated pair passes between them is at least

\[\Pr_{s,s' \sim T_\rho}[s \in A, s' \in B] \geq \Pr[A]^{O(1)} \Pr[B]^{O(1)}.\]

Our results hold under weak spectral assumptions on $X$. Namely we prove

exponential concentration of measure for any complex below the `Trickling-Down

Threshold' (beyond which concentration may be arbitrarily poor), and optimal

concentration for $\sqrt{k}$-skeletons of such complexes. We also show optimal

bounds for the top dimension of stronger HDX among other settings. We leverage

our inequalities to prove several new agreement testing theorems on high

dimensional expanders, including a new 99%-regime test for subsets, and a

variant of the `Z-test' achieving inverse exponential soundness under the

stronger assumption of $\ell_\infty$-expansion. The latter gives rise to the

first optimal testers beyond the complete complex and products, a stepping

stone toward the use of HDX in strong soundness PCPs. We also give applications

within expansion, analysis, combinatorics, and coding theory, including a proof

that two-sided HDX have optimal geometric overlap (giving the first explicit

bounded-degree construction), near-optimal double samplers, new

super-exponential degree lower bounds for certain HDX, distance-amplified

list-decodable and locally testable codes, a Frankl-R\"odl Theorem and more.

We prove optimal concentration of measure for lifted functions on high

dimensional expanders (HDX). Let $X$ be a $k$-dimensional HDX. We show for any

$i\leq k$ and $f:X(i)\to [0,1]$: \[\Pr_{s\in

X(k)}\left[\left|\underset{{t\subseteq

s}}{\mathbb{E}}[f(t)]-\mu\right|\geq\varepsilon\right]\leq

exp\left(-\varepsilon^2\frac{k}{i}\right).\] Using this fact, we prove that

high dimensional expanders are reverse hypercontractive, a powerful functional

inequality from discrete analysis implying that for any sets $A,B \subset

X(k)$, the probability a $\rho$-correlated pair passes between them is at least

\[\Pr_{s,s' \sim T_\rho}[s \in A, s' \in B] \geq \Pr[A]^{O(1)} \Pr[B]^{O(1)}.\]

Our results hold under weak spectral assumptions on $X$. Namely we prove

exponential concentration of measure for any complex below the `Trickling-Down

Threshold' (beyond which concentration may be arbitrarily poor), and optimal

concentration for $\sqrt{k}$-skeletons of such complexes. We also show optimal

bounds for the top dimension of stronger HDX among other settings. We leverage

our inequalities to prove several new agreement testing theorems on high

dimensional expanders, including a new 99%-regime test for subsets, and a

variant of the `Z-test' achieving inverse exponential soundness under the

stronger assumption of $\ell_\infty$-expansion. The latter gives rise to the

first optimal testers beyond the complete complex and products, a stepping

stone toward the use of HDX in strong soundness PCPs. We also give applications

within expansion, analysis, combinatorics, and coding theory, including a proof

that two-sided HDX have optimal geometric overlap (giving the first explicit

bounded-degree construction), near-optimal double samplers, new

super-exponential degree lower bounds for certain HDX, distance-amplified

list-decodable and locally testable codes, a Frankl-R\"odl Theorem and more.

The ZH calculus is a graphical language for quantum computation reasoning.

The phase-free variant offers a simple set of generators that guarantee

universality. ZH calculus is effective in MBQC and analysis of quantum circuits

constructed with the universal gate set Toffoli+H. While circuits naturally

translate to ZH diagrams, finding an ancilla-free circuit equivalent to a given

diagram is hard. Here, we show that circuit extraction for phase-free ZH

calculus is ${\mathord{\#}\mathrm P}$-hard, extending the existing result for

ZX calculus. Another problem believed to be hard is comparing whether two

diagrams represent the same process. We show that two closely related problems

are $\mathrm{NP}^{\mathord{\#}\mathrm P}$-complete. The first problem is: given

two processes represented as diagrams, determine the existence of a

computational basis state on which they equalize. The second problem is

checking whether the matrix representation of a given diagram contains an entry

equal to a given number. Our proof adapts the proof of Cook-Levin theorem to a

reduction from a non-deterministic Turing Machine with access to

${\mathord{\#}\mathrm P}$ oracle.

The ZH calculus is a graphical language for quantum computation reasoning.

The phase-free variant offers a simple set of generators that guarantee

universality. ZH calculus is effective in MBQC and analysis of quantum circuits

constructed with the universal gate set Toffoli+H. While circuits naturally

translate to ZH diagrams, finding an ancilla-free circuit equivalent to a given

diagram is hard. Here, we show that circuit extraction for phase-free ZH

calculus is ${\mathord{\#}\mathrm P}$-hard, extending the existing result for

ZX calculus. Another problem believed to be hard is comparing whether two

diagrams represent the same process. We show that two closely related problems

are $\mathrm{NP}^{\mathord{\#}\mathrm P}$-complete. The first problem is: given

two processes represented as diagrams, determine the existence of a

computational basis state on which they equalize. The second problem is

checking whether the matrix representation of a given diagram contains an entry

equal to a given number. Our proof adapts the proof of Cook-Levin theorem to a

reduction from a non-deterministic Turing Machine with access to

${\mathord{\#}\mathrm P}$ oracle.

We design polynomial size, constant depth (namely, $\mathsf{AC}^0$)

arithmetic formulae for the greatest common divisor (GCD) of two polynomials,

as well as the related problems of the discriminant, resultant, B\'ezout

coefficients, squarefree decomposition, and the inversion of structured

matrices like Sylvester and B\'ezout matrices. Our GCD algorithm extends to any

number of polynomials. Previously, the best known arithmetic formulae for these

problems required super-polynomial size, regardless of depth.

These results are based on new algorithmic techniques to compute various

symmetric functions in the roots of polynomials, as well as manipulate the

multiplicities of these roots, without having access to them. These techniques

allow $\mathsf{AC}^0$ computation of a large class of linear and polynomial

algebra problems, which include the above as special cases.

We extend these techniques to problems whose inputs are multivariate

polynomials, which are represented by $\mathsf{AC}^0$ arithmetic circuits. Here

too we solve problems such as computing the GCD and squarefree decomposition in

$\mathsf{AC}^0$.

We design polynomial size, constant depth (namely, $\mathsf{AC}^0$)

arithmetic formulae for the greatest common divisor (GCD) of two polynomials,

as well as the related problems of the discriminant, resultant, B\'ezout

coefficients, squarefree decomposition, and the inversion of structured

matrices like Sylvester and B\'ezout matrices. Our GCD algorithm extends to any

number of polynomials. Previously, the best known arithmetic formulae for these

problems required super-polynomial size, regardless of depth.

These results are based on new algorithmic techniques to compute various

symmetric functions in the roots of polynomials, as well as manipulate the

multiplicities of these roots, without having access to them. These techniques

allow $\mathsf{AC}^0$ computation of a large class of linear and polynomial

algebra problems, which include the above as special cases.

We extend these techniques to problems whose inputs are multivariate

polynomials, which are represented by $\mathsf{AC}^0$ arithmetic circuits. Here

too we solve problems such as computing the GCD and squarefree decomposition in

$\mathsf{AC}^0$.

Authors: Felicia Lucke, Ali Momeni, Daniël Paulusma, Siani Smith

The $d$-Cut problem is to decide if a graph has an edge cut such that each

vertex has at most $d$ neighbours at the opposite side of the cut. If $d=1$, we

obtain the intensively studied Matching Cut problem. The $d$-Cut problem has

been studied as well, but a systematic study for special graph classes was

lacking. We initiate such a study and consider classes of bounded diameter,

bounded radius and $H$-free graphs. We prove that for all $d\geq 2$, $d$-Cut is

polynomial-time solvable for graphs of diameter $2$, $(P_3+P_4)$-free graphs

and $P_5$-free graphs. These results extend known results for $d=1$. However,

we also prove several NP-hardness results for $d$-Cut that contrast known

polynomial-time results for $d=1$. Our results lead to full dichotomies for

bounded diameter and bounded radius and to almost-complete dichotomies for

$H$-free graphs.

The $d$-Cut problem is to decide if a graph has an edge cut such that each

vertex has at most $d$ neighbours at the opposite side of the cut. If $d=1$, we

obtain the intensively studied Matching Cut problem. The $d$-Cut problem has

been studied as well, but a systematic study for special graph classes was

lacking. We initiate such a study and consider classes of bounded diameter,

bounded radius and $H$-free graphs. We prove that for all $d\geq 2$, $d$-Cut is

polynomial-time solvable for graphs of diameter $2$, $(P_3+P_4)$-free graphs

and $P_5$-free graphs. These results extend known results for $d=1$. However,

we also prove several NP-hardness results for $d$-Cut that contrast known

polynomial-time results for $d=1$. Our results lead to full dichotomies for

bounded diameter and bounded radius and to almost-complete dichotomies for

$H$-free graphs.

We study the complexity of approximating the permanent of a positive

semidefinite matrix $A\in \mathbb{C}^{n\times n}$.

1. We design a new approximation algorithm for $\mathrm{per}(A)$ with

approximation ratio $e^{(0.9999 + \gamma)n}$, exponentially improving upon the

current best bound of $e^{(1+\gamma-o(1))n}$ [AGOS17,YP22]. Here, $\gamma

\approx 0.577$ is Euler's constant.

2. We prove that it is NP-hard to approximate $\mathrm{per}(A)$ within a

factor $e^{(\gamma-\epsilon)n}$ for any $\epsilon>0$. This is the first

exponential hardness of approximation for this problem. Along the way, we prove

optimal hardness of approximation results for the $\|\cdot\|_{2\to q}$ ``norm''

problem of a matrix for all $-1 < q < 2$.

We study the complexity of approximating the permanent of a positive

semidefinite matrix $A\in \mathbb{C}^{n\times n}$.

1. We design a new approximation algorithm for $\mathrm{per}(A)$ with

approximation ratio $e^{(0.9999 + \gamma)n}$, exponentially improving upon the

current best bound of $e^{(1+\gamma-o(1))n}$ [AGOS17,YP22]. Here, $\gamma

\approx 0.577$ is Euler's constant.

2. We prove that it is NP-hard to approximate $\mathrm{per}(A)$ within a

factor $e^{(\gamma-\epsilon)n}$ for any $\epsilon>0$. This is the first

exponential hardness of approximation for this problem. Along the way, we prove

optimal hardness of approximation results for the $\|\cdot\|_{2\to q}$ ``norm''

problem of a matrix for all $-1 < q < 2$.

Authors: Toluwanimi O. Odemuyiwa, Joel S. Emer, John D. Owens

In this work, we propose a unified abstraction for graph algorithms: the

Extended General Einsums language, or EDGE. The EDGE language expresses graph

algorithms in the language of tensor algebra, providing a rigorous, succinct,

and expressive mathematical framework. EDGE leverages two ideas: (1) the

well-known foundations provided by the graph-matrix duality, where a graph is

simply a 2D tensor, and (2) the power and expressivity of Einsum notation in

the tensor algebra world. In this work, we describe our design goals for EDGE

and walk through the extensions we add to Einsums to support more complex

operations common in graph algorithms. Additionally, we provide a few examples

of how to express graph algorithms in our proposed notation. We hope that a

single, mathematical notation for graph algorithms will (1) allow researchers

to more easily compare different algorithms and different implementations of a

graph algorithm; (2) enable developers to factor complexity by separating the

concerns of what to compute (described with the extended Einsum notation) from

the lower level details of how to compute; and (3) enable the discovery of

different algorithmic variants of a problem through algebraic manipulations and

transformations on a given EDGE expression.

In this work, we propose a unified abstraction for graph algorithms: the

Extended General Einsums language, or EDGE. The EDGE language expresses graph

algorithms in the language of tensor algebra, providing a rigorous, succinct,

and expressive mathematical framework. EDGE leverages two ideas: (1) the

well-known foundations provided by the graph-matrix duality, where a graph is

simply a 2D tensor, and (2) the power and expressivity of Einsum notation in

the tensor algebra world. In this work, we describe our design goals for EDGE

and walk through the extensions we add to Einsums to support more complex

operations common in graph algorithms. Additionally, we provide a few examples

of how to express graph algorithms in our proposed notation. We hope that a

single, mathematical notation for graph algorithms will (1) allow researchers

to more easily compare different algorithms and different implementations of a

graph algorithm; (2) enable developers to factor complexity by separating the

concerns of what to compute (described with the extended Einsum notation) from

the lower level details of how to compute; and (3) enable the discovery of

different algorithmic variants of a problem through algebraic manipulations and

transformations on a given EDGE expression.

A set family ${\cal F}$ is called intersecting if every two members of ${\cal

F}$ intersect, and it is called uniform if all members of ${\cal F}$ share a

common size. A uniform family ${\cal F} \subseteq \binom{[n]}{k}$ of

$k$-subsets of $[n]$ is $\varepsilon$-far from intersecting if one has to

remove more than $\varepsilon \cdot \binom{n}{k}$ of the sets of ${\cal F}$ to

make it intersecting. We study the property testing problem that given query

access to a uniform family ${\cal F} \subseteq \binom{[n]}{k}$, asks to

distinguish between the case that ${\cal F}$ is intersecting and the case that

it is $\varepsilon$-far from intersecting. We prove that for every fixed

integer $r$, the problem admits a non-adaptive two-sided error tester with

query complexity $O(\frac{\ln n}{\varepsilon})$ for $\varepsilon \geq \Omega(

(\frac{k}{n})^r)$ and a non-adaptive one-sided error tester with query

complexity $O(\frac{\ln k}{\varepsilon})$ for $\varepsilon \geq \Omega(

(\frac{k^2}{n})^r)$. The query complexities are optimal up to the logarithmic

terms. For $\varepsilon \geq \Omega( (\frac{k^2}{n})^2)$, we further provide a

non-adaptive one-sided error tester with optimal query complexity of

$O(\frac{1}{\varepsilon})$. Our findings show that the query complexity of the

problem differs substantially from that of testing intersectingness of

non-uniform families, studied recently by Chen, De, Li, Nadimpalli, and

Servedio (ITCS, 2024).

A set family ${\cal F}$ is called intersecting if every two members of ${\cal

F}$ intersect, and it is called uniform if all members of ${\cal F}$ share a

common size. A uniform family ${\cal F} \subseteq \binom{[n]}{k}$ of

$k$-subsets of $[n]$ is $\varepsilon$-far from intersecting if one has to

remove more than $\varepsilon \cdot \binom{n}{k}$ of the sets of ${\cal F}$ to

make it intersecting. We study the property testing problem that given query

access to a uniform family ${\cal F} \subseteq \binom{[n]}{k}$, asks to

distinguish between the case that ${\cal F}$ is intersecting and the case that

it is $\varepsilon$-far from intersecting. We prove that for every fixed

integer $r$, the problem admits a non-adaptive two-sided error tester with

query complexity $O(\frac{\ln n}{\varepsilon})$ for $\varepsilon \geq \Omega(

(\frac{k}{n})^r)$ and a non-adaptive one-sided error tester with query

complexity $O(\frac{\ln k}{\varepsilon})$ for $\varepsilon \geq \Omega(

(\frac{k^2}{n})^r)$. The query complexities are optimal up to the logarithmic

terms. For $\varepsilon \geq \Omega( (\frac{k^2}{n})^2)$, we further provide a

non-adaptive one-sided error tester with optimal query complexity of

$O(\frac{1}{\varepsilon})$. Our findings show that the query complexity of the

problem differs substantially from that of testing intersectingness of

non-uniform families, studied recently by Chen, De, Li, Nadimpalli, and

Servedio (ITCS, 2024).

Given functions $f$ and $g$ defined on the subset lattice of order $n$, their

min-sum subset convolution, defined for all $S \subseteq [n]$ as \[

(f \star g)(S) = \min_{T \subseteq S}\:\big(f(T) + g(S \setminus T)\big), \]

is a fundamental tool in parameterized algorithms. However, since its na\"ive

$O(3^n)$-time evaluation is also the fastest known, it has been used only in

settings where the input functions have a bounded integer range $\{-M, \ldots,

M\}$. In this case, the running time becomes $\tilde O(2^n M)$ by resorting to

fast subset convolution in the sum-product ring. This is disadvantageous due to

the dependence on $M$, limiting its practicality.

In this light, we study whether the problem admits an $(1 +

\varepsilon)$-approximation scheme in time independent of $M$. Our main result

is the first $\tilde O(2^\frac{3n}{2} / \sqrt{\varepsilon})$-time algorithm for

the $(1 + \varepsilon)$-approximate min-sum subset convolution. To show its

applicability, we present $(1 + \varepsilon)$-approximation schemes in the same

exponential time bound for several NP-hard problems using this convolution,

such as the minimum-cost $k$-coloring problem -- in time $\tilde

O(2^\frac{3n}{2} / \sqrt{\varepsilon})$, and the prize-collecting Steiner tree

problem -- in time $\tilde O(2^\frac{3s^+}{2} / \sqrt{\varepsilon})$, where $n$

is the number of vertices and $s^+$ is the number of proper potential

terminals. We also discuss two other applications in computational biology.

Our algorithms lie at the intersection of two lines of research that have

been considered separately: $\textit{sequence}$ and $\textit{subset}$

convolutions in semi-rings. In particular, we extend the recent framework of

Bringmann, K\"unnemann, and W\k{e}grzycki [STOC 2019] to the context of subset

convolutions.

Given functions $f$ and $g$ defined on the subset lattice of order $n$, their

min-sum subset convolution, defined for all $S \subseteq [n]$ as \[

(f \star g)(S) = \min_{T \subseteq S}\:\big(f(T) + g(S \setminus T)\big), \]

is a fundamental tool in parameterized algorithms. However, since its na\"ive

$O(3^n)$-time evaluation is also the fastest known, it has been used only in

settings where the input functions have a bounded integer range $\{-M, \ldots,

M\}$. In this case, the running time becomes $\tilde O(2^n M)$ by resorting to

fast subset convolution in the sum-product ring. This is disadvantageous due to

the dependence on $M$, limiting its practicality.

In this light, we study whether the problem admits an $(1 +

\varepsilon)$-approximation scheme in time independent of $M$. Our main result

is the first $\tilde O(2^\frac{3n}{2} / \sqrt{\varepsilon})$-time algorithm for

the $(1 + \varepsilon)$-approximate min-sum subset convolution. To show its

applicability, we present $(1 + \varepsilon)$-approximation schemes in the same

exponential time bound for several NP-hard problems using this convolution,

such as the minimum-cost $k$-coloring problem -- in time $\tilde

O(2^\frac{3n}{2} / \sqrt{\varepsilon})$, and the prize-collecting Steiner tree

problem -- in time $\tilde O(2^\frac{3s^+}{2} / \sqrt{\varepsilon})$, where $n$

is the number of vertices and $s^+$ is the number of proper potential

terminals. We also discuss two other applications in computational biology.

Our algorithms lie at the intersection of two lines of research that have

been considered separately: $\textit{sequence}$ and $\textit{subset}$

convolutions in semi-rings. In particular, we extend the recent framework of

Bringmann, K\"unnemann, and W\k{e}grzycki [STOC 2019] to the context of subset

convolutions.

In this expository note we show that the learning parities with noise (LPN)

assumption is robust to weak dependencies in the noise distribution of small

batches of samples. This provides a partial converse to the linearization

technique of [AG11]. The material in this note is drawn from a recent work by

the authors [GMR24], where the robustness guarantee was a key component in a

cryptographic separation between reinforcement learning and supervised

learning.

In this expository note we show that the learning parities with noise (LPN)

assumption is robust to weak dependencies in the noise distribution of small

batches of samples. This provides a partial converse to the linearization

technique of [AG11]. The material in this note is drawn from a recent work by

the authors [GMR24], where the robustness guarantee was a key component in a

cryptographic separation between reinforcement learning and supervised

learning.

We give a distribution-free testing algorithm for decision lists with

$\tilde{O}(n^{11/12}/\varepsilon^3)$ queries. This is the first sublinear

algorithm for this problem, which shows that, unlike halfspaces, testing is

strictly easier than learning for decision lists. Complementing the algorithm,

we show that any distribution-free tester for decision lists must make

$\tilde{\Omega}(\sqrt{n})$ queries, or draw $\tilde{\Omega}(n)$ samples when

the algorithm is sample-based.

We give a distribution-free testing algorithm for decision lists with

$\tilde{O}(n^{11/12}/\varepsilon^3)$ queries. This is the first sublinear

algorithm for this problem, which shows that, unlike halfspaces, testing is

strictly easier than learning for decision lists. Complementing the algorithm,

we show that any distribution-free tester for decision lists must make

$\tilde{\Omega}(\sqrt{n})$ queries, or draw $\tilde{\Omega}(n)$ samples when

the algorithm is sample-based.

Authors: Nicole Immorlica, Brendan Lucier, Markus Mobius, James Siderius

We introduce a model of online algorithms subject to strict constraints on

data retention. An online learning algorithm encounters a stream of data

points, one per round, generated by some stationary process. Crucially, each

data point can request that it be removed from memory $m$ rounds after it

arrives. To model the impact of removal, we do not allow the algorithm to store

any information or calculations between rounds other than a subset of the data

points (subject to the retention constraints). At the conclusion of the stream,

the algorithm answers a statistical query about the full dataset. We ask: what

level of performance can be guaranteed as a function of $m$?

We illustrate this framework for multidimensional mean estimation and linear

regression problems. We show it is possible to obtain an exponential

improvement over a baseline algorithm that retains all data as long as

possible. Specifically, we show that $m = \textsc{Poly}(d, \log(1/\epsilon))$

retention suffices to achieve mean squared error $\epsilon$ after observing

$O(1/\epsilon)$ $d$-dimensional data points. This matches the error bound of

the optimal, yet infeasible, algorithm that retains all data forever. We also

show a nearly matching lower bound on the retention required to guarantee error

$\epsilon$. One implication of our results is that data retention laws are

insufficient to guarantee the right to be forgotten even in a non-adversarial

world in which firms merely strive to (approximately) optimize the performance

of their algorithms.

Our approach makes use of recent developments in the multidimensional random

subset sum problem to simulate the progression of stochastic gradient descent

under a model of adversarial noise, which may be of independent interest.

We introduce a model of online algorithms subject to strict constraints on

data retention. An online learning algorithm encounters a stream of data

points, one per round, generated by some stationary process. Crucially, each

data point can request that it be removed from memory $m$ rounds after it

arrives. To model the impact of removal, we do not allow the algorithm to store

any information or calculations between rounds other than a subset of the data

points (subject to the retention constraints). At the conclusion of the stream,

the algorithm answers a statistical query about the full dataset. We ask: what

level of performance can be guaranteed as a function of $m$?

We illustrate this framework for multidimensional mean estimation and linear

regression problems. We show it is possible to obtain an exponential

improvement over a baseline algorithm that retains all data as long as

possible. Specifically, we show that $m = \textsc{Poly}(d, \log(1/\epsilon))$

retention suffices to achieve mean squared error $\epsilon$ after observing

$O(1/\epsilon)$ $d$-dimensional data points. This matches the error bound of

the optimal, yet infeasible, algorithm that retains all data forever. We also

show a nearly matching lower bound on the retention required to guarantee error

$\epsilon$. One implication of our results is that data retention laws are

insufficient to guarantee the right to be forgotten even in a non-adversarial

world in which firms merely strive to (approximately) optimize the performance

of their algorithms.

Our approach makes use of recent developments in the multidimensional random

subset sum problem to simulate the progression of stochastic gradient descent

under a model of adversarial noise, which may be of independent interest.

Authors: Gabriel Chuang, Oussama Hanguir, Clifford Stein

In the process of redistricting, one important metric is the number of

competitive districts, that is, districts where both parties have a reasonable

chance of winning a majority of votes. Competitive districts are important for

achieving proportionality, responsiveness, and other desirable qualities; some

states even directly list competitiveness in their legally-codified districting

requirements. In this work, we discuss the problem of drawing plans with at

least a fixed number of competitive districts. In addition to the standard,

``vote-band'' measure of competitivenesss (i.e., how close was the last

election?), we propose a measure that explicitly considers ``swing voters'' -

the segment of the population that may choose to vote either way, or not vote

at all, in a given election. We present two main, contrasting results. First,

from a computational complexity perspective, we show that the task of drawing

plans with competitive districts is NP-hard, even on very natural instances

where the districting task itself is easy (e.g., small rectangular grids of

population-balanced cells). Second, however, we show that a simple

hill-climbing procedure can in practice find districtings on real states in

which all the districts are competitive. We present the results of the latter

on the precinct-level graphs of the U.S. states of North Carolina and Arizona,

and discuss trade-offs between competitiveness and other desirable qualities.

In the process of redistricting, one important metric is the number of

competitive districts, that is, districts where both parties have a reasonable

chance of winning a majority of votes. Competitive districts are important for

achieving proportionality, responsiveness, and other desirable qualities; some

states even directly list competitiveness in their legally-codified districting

requirements. In this work, we discuss the problem of drawing plans with at

least a fixed number of competitive districts. In addition to the standard,

``vote-band'' measure of competitivenesss (i.e., how close was the last

election?), we propose a measure that explicitly considers ``swing voters'' -

the segment of the population that may choose to vote either way, or not vote

at all, in a given election. We present two main, contrasting results. First,

from a computational complexity perspective, we show that the task of drawing

plans with competitive districts is NP-hard, even on very natural instances

where the districting task itself is easy (e.g., small rectangular grids of

population-balanced cells). Second, however, we show that a simple

hill-climbing procedure can in practice find districtings on real states in

which all the districts are competitive. We present the results of the latter

on the precinct-level graphs of the U.S. states of North Carolina and Arizona,

and discuss trade-offs between competitiveness and other desirable qualities.

The Traveling Tournament Problem (TTP) is a well-known benchmark problem in

the field of tournament timetabling, which asks us to design a double

round-robin schedule such that each pair of teams plays one game in each

other's home venue, minimizing the total distance traveled by all $n$ teams

($n$ is even). TTP-$k$ is the problem with one more constraint that each team

can have at most $k$-consecutive home games or away games. In this paper, we

investigate schedules for TTP-$k$ and analyze the approximation ratio of the

solutions. Most previous schedules were constructed based on a Hamiltonian

cycle of the graph. We will propose a novel construction based on a $k$-cycle

packing. Then, combining our $k$-cycle packing schedule with the Hamiltonian

cycle schedule, we obtain improved approximation ratios for TTP-$k$ with deep

analysis. The case where $k=3$, TTP-3, is one of the most investigated cases.

We improve the approximation ratio of TTP-3 from $(1.667+\varepsilon)$ to

$(1.598+\varepsilon)$, for any $\varepsilon>0$. For TTP-$4$, we improve the

approximation ratio from $(1.750+\varepsilon)$ to $(1.700+\varepsilon)$. By a

refined analysis of the Hamiltonian cycle construction, we also improve the

approximation ratio of TTP-$k$ from $(\frac{5k-7}{2k}+\varepsilon)$ to

$(\frac{5k^2-4k+3}{2k(k+1)}+\varepsilon)$ for any constant $k\geq 5$. Our

methods can be extended to solve a variant called LDTTP-$k$ (TTP-$k$ where all

teams are allocated on a straight line). We show that the $k$-cycle packing

construction can achieve an approximation ratio of

$(\frac{3k-3}{2k-1}+\varepsilon)$, which improves the approximation ratio of

LDTTP-3 from $4/3$ to $(6/5+\varepsilon)$.

The Traveling Tournament Problem (TTP) is a well-known benchmark problem in

the field of tournament timetabling, which asks us to design a double

round-robin schedule such that each pair of teams plays one game in each

other's home venue, minimizing the total distance traveled by all $n$ teams

($n$ is even). TTP-$k$ is the problem with one more constraint that each team

can have at most $k$-consecutive home games or away games. In this paper, we

investigate schedules for TTP-$k$ and analyze the approximation ratio of the